For most Singapore companies limited by shares, one fully paid ordinary share of S$1 is sufficient at the point of incorporation.

This means that a company can generally be incorporated with S$1 in paid-up capital, provided that it is not subject to a separate licensing, grant or industry requirement.

However, the legal minimum is not necessarily the most suitable amount for every company. Paid-up capital may affect licensing applications, grant eligibility, tender requirements and how the company is funded during its early stages.

The amount should therefore be based on what the company requires, rather than an arbitrary figure chosen only for appearance.

What Is Paid-Up Capital?

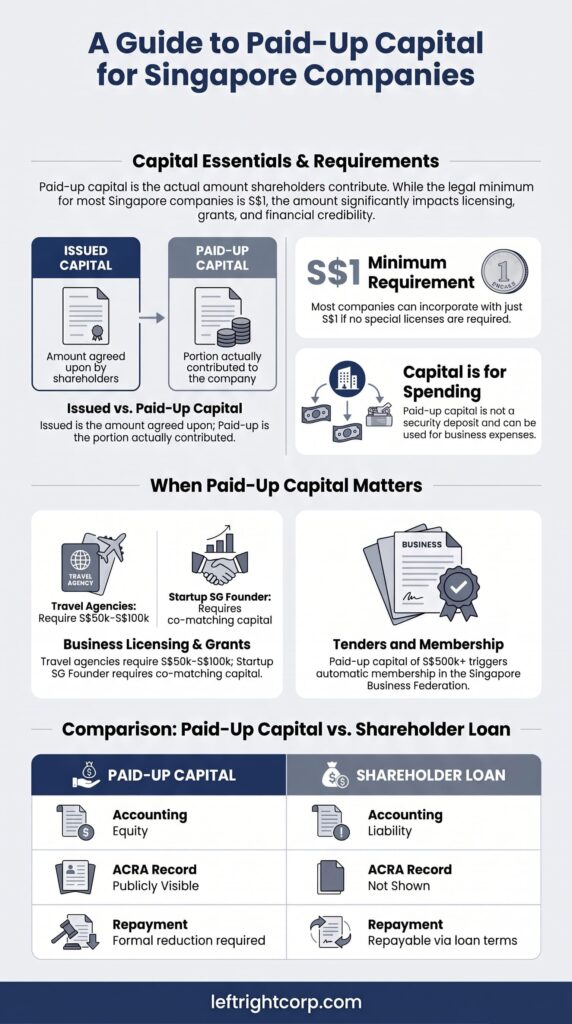

Paid-up capital is the amount that shareholders have actually contributed to the company in exchange for shares.

For example:

- If the company allots 1 ordinary share for S$1 and the shareholder pays S$1, the paid-up capital is S$1

- If the company allots 10,000 shares for a total of S$10,000 and the full amount is paid, the paid-up capital is S$10,000

- If shares are only partially paid, the unpaid portion remains outstanding from the shareholder

Once contributed, the money belongs to the company. It is no longer the shareholder’s personal money, even where the shareholder is also the sole director.

The funds may be used for legitimate company expenses such as rent, equipment, salaries, software, professional fees, inventory and marketing.

View ACRA’s guidance on share capital and paid-up capital.

Issued Share Capital and Paid-Up Capital

Issued share capital and paid-up capital are related, but they do not always mean the same thing.

| Term | Meaning |

|---|---|

| Issued share capital | The amount that shareholders have agreed to contribute for the shares allotted to them |

| Paid-up capital | The portion of the issued share capital that the shareholders have actually paid |

| Unpaid share capital | The amount that remains payable by shareholders on partially paid shares |

Most small Singapore companies issue fully paid shares. Their issued share capital and paid-up capital will therefore be the same.

A company should not declare an amount as paid-up capital unless the agreed consideration has genuinely been provided by the shareholder and properly recorded in the company’s accounts.

Must the Paid-Up Capital Remain in the Bank Account?

No. Paid-up capital is not a security deposit that must remain untouched in the company’s bank account.

Once the funds have been contributed, the company may use them for its business operations. The company does not need to maintain a bank balance equal to the amount shown as paid-up capital.

For example, a company may receive S$10,000 in paid-up capital and subsequently spend S$6,000 on equipment, rent and professional fees. Its paid-up capital remains S$10,000 even though only S$4,000 may remain in the bank.

Paid-up capital is not the same as cash available: The amount shown on the company’s ACRA record reflects capital contributed by shareholders. It does not confirm how much cash the company currently holds, whether the company is profitable, or whether it can pay its debts.

The funds must nevertheless be used for the company’s purposes. A shareholder cannot simply withdraw the capital for personal use because they originally contributed it.

Does Paid-Up Capital Affect Tax or Personal Liability?

Corporate income tax

A shareholder’s capital contribution is not business revenue. Increasing the company’s paid-up capital does not by itself increase or reduce the company’s corporate income tax.

Corporate income tax is generally calculated based on the company’s taxable income after the relevant deductions, exemptions and tax adjustments.

Shareholder liability

For a company limited by shares, a shareholder’s liability as shareholder is generally limited to any amount remaining unpaid on their shares.

If the shares are fully paid, the shareholder would not ordinarily be required to contribute further merely because the company owes money to its creditors.

This does not protect a director from personal liability arising from matters such as a personal guarantee, breach of director duties, fraud or other misconduct. The protection arising from limited liability should not be confused with a director’s separate legal responsibilities.

When Does Paid-Up Capital Matter?

1. Business licences and regulated activities

Some businesses must maintain a prescribed level of paid-up capital before they may obtain or retain a licence.

One example is a licensed travel agency. The Singapore Tourism Board currently requires a minimum paid-up capital and net value of:

- S$50,000 for a Niche Travel Agent Licence

- S$100,000 for a General Travel Agent Licence

Other regulated sectors and registration schemes may impose different capital or financial requirements.

If the company requires a licence, the applicable conditions should be checked before deciding on the initial share capital.

View the Singapore Tourism Board’s Travel Agent Licence requirements.

2. Grants and funding programmes

Certain government funding programmes require the founders or shareholders to inject co-matching capital into the company.

For example, the Startup SG Founder programme requires applicants to contribute co-matching paid-up capital based on the grant amount applied for. Part of the required capital must already be reflected in the company’s ACRA records at the application stage.

This does not mean that all government grants require a particular level of paid-up capital. Each scheme has its own eligibility and funding conditions.

Companies planning to apply for a specific grant should review the current requirements before incorporation or before submitting the application.

View the current Startup SG Founder application requirements.

3. Tenders and commercial contracts

Some government tenders, contractor registrations, supplier panels and private procurement processes specify minimum financial requirements.

These may refer to paid-up capital, net worth, turnover, track record or a combination of several financial measures.

There is no general rule that every company dealing with corporate customers must have S$10,000, S$50,000 or any other fixed amount of capital. The requirement depends on the contract, tender or registration scheme concerned.

4. Banks, landlords and business counterparties

The company’s paid-up capital appears in its ACRA records and may be reviewed by banks, landlords, customers and suppliers as part of their due diligence.

A higher amount may indicate that shareholders have committed more funding to the company. However, it should not be treated as proof that the money remains available or that the company is financially strong.

A counterparty assessing the company properly may also consider its financial statements, bank records, operating history, guarantees, cash flow and credit profile.

Similarly, a bank account’s initial deposit or minimum balance requirement is separate from the company’s paid-up capital. Funds placed into the company may be recorded as share capital or as a shareholder loan, depending on the actual arrangement and supporting documents.

5. Singapore Business Federation membership

A company with paid-up capital of S$500,000 or more automatically becomes a member of the Singapore Business Federation.

This threshold should be considered where a company is planning a substantial increase in capital, particularly where the increase brings the company to or above S$500,000.

Does EntrePass Require S$50,000 in Paid-Up Capital?

No. EntrePass applicants are no longer required to maintain S$50,000 in paid-up capital.

The previous S$50,000 requirement was removed in 2017. Under the current criteria, an applicant must generally:

- Have started or intend to start a Singapore private limited company

- Hold at least 30% of the company

- Operate a business that is venture-backed or owns innovative technologies

- Meet at least one of MOM’s entrepreneur, innovator or investor criteria

Paid-up capital may still form part of the overall commercial background of the company, but MOM does not prescribe S$50,000 as a current minimum EntrePass requirement.

Do not rely on older incorporation guides: Articles that continue to state that EntrePass applicants must have S$50,000 in paid-up capital are referring to a requirement that was removed several years ago.

View the current EntrePass eligibility criteria.

Paid-Up Capital vs Shareholder Loan

A shareholder may fund the company through share capital, a shareholder loan, or a combination of both.

They are recorded differently and have different legal consequences.

| Paid-Up Capital | Shareholder Loan | |

|---|---|---|

| Accounting classification | Equity | Liability owed by the company |

| Shares issued | Yes | No |

| Can be repaid directly | Not as an ordinary repayment to the shareholder | Generally repayable according to the loan arrangement |

| Shown as paid-up capital on ACRA | Yes | No |

| Effect on ownership | May affect the number of shares and ownership percentages | Does not by itself change share ownership |

A shareholder loan provides greater repayment flexibility because the company may repay the amount when it has sufficient funds and the repayment is properly supported.

Share capital provides permanent equity funding and may be preferable where the company requires capital for a licence, grant, tender or investment arrangement.

Where there is more than one shareholder, any additional share allotment should also be reviewed for its effect on voting rights and ownership percentages.

How Much Paid-Up Capital Should You Start With?

There is no standard amount that is suitable for every company.

A practical decision can be made by considering the following:

Check for a prescribed requirement

First, confirm whether the company’s licence, grant, tender, registration scheme or investor agreement requires a particular amount.

Where a minimum applies, the company should satisfy that requirement rather than relying on the general S$1 incorporation threshold.

Estimate the amount the company will actually use

Consider the amount that the shareholders genuinely intend to contribute for the company’s initial expenses.

This may include:

- Incorporation and professional fees

- Rental deposits

- Equipment and software

- Initial inventory

- Marketing expenses

- Several months of operating costs

It is generally better to choose an amount that reflects the company’s actual funding arrangement than to register a large figure purely to make the company appear more established.

Consider whether part of the funding should be a loan

Where the shareholder expects the company to repay part of the funding later, it may be appropriate to structure that portion as a shareholder loan rather than share capital.

The intended treatment should be decided and documented when the money is introduced, rather than being changed informally afterwards.

Consider the ownership structure

For companies with several founders or investors, the number and class of shares may be more important than the headline dollar amount.

The share structure should accurately reflect the agreed ownership, voting rights and economic rights of each shareholder.

Practical recommendation: For a straightforward service company with no special capital requirement, S$1 is legally sufficient. However, the shareholders may choose to register the amount they genuinely intend to contribute for the company’s initial operating expenses. There is usually little benefit in declaring a larger amount that has not actually been paid.

Can Paid-Up Capital Be Increased Later?

Yes. A company may increase its paid-up capital after incorporation.

This is commonly done by allotting additional shares for cash. The process generally involves:

- Obtaining the members’ prior approval for the company to issue shares

- Having the directors decide the number, class, issue price and other terms of the allotment

- Receiving the agreed payment or other consideration

- Filing the return of allotment through ACRA’s Bizfile

- Updating the company’s statutory records and accounting entries

For a private company, the allotment generally takes effect when ACRA updates the company’s Electronic Register of Members following the filing. The allotment should therefore not be backdated.

If the company already has partially paid shares, paid-up capital may also be increased when shareholders pay the outstanding amount on those shares. A separate notice must be filed with ACRA to update the paid-up amount.

New shares issued to one shareholder may dilute the ownership percentages of the other shareholders. The company should review the existing share rights, Constitution and any shareholders’ agreement before proceeding.

View ACRA’s share allotment filing guidance.

Can Paid-Up Capital Be Reduced Later?

Yes, but reducing share capital is considerably more involved than increasing it.

A company may carry out a capital reduction for reasons such as returning excess capital, cancelling capital no longer represented by assets, simplifying its capital structure or eliminating accumulated losses.

Under the members’ approval route, the process generally involves:

- Passing a special resolution

- Preparing the required solvency declaration

- Filing the special resolution and proposed reduction with ACRA

- Allowing a six-week period during which creditors may apply to Court to object

- Filing the final capital reduction transaction if no objection prevents the reduction

The final filing under this route must generally be made between six and eight weeks after the special resolution. The reduction takes effect after the filing is successfully submitted.

A capital reduction may also be carried out through a Court-approved process.

Because the procedure and consequences depend on the purpose of the reduction, it should be properly reviewed before any money is returned to shareholders.

View ACRA’s guidance on reducing share capital.

Common Questions

Is S$1 paid-up capital legal?

For an ordinary Singapore company limited by shares, one fully paid S$1 share is generally sufficient at incorporation. A higher amount may be required where the company is subject to a particular licence, grant, tender or regulatory condition.

Does a company with S$1 capital look suspicious?

S$1 capital is common among newly incorporated companies and is not by itself evidence of anything improper. A bank, landlord or customer may nevertheless request further information about the company’s business, funding and financial position.

Can the company spend its paid-up capital?

Yes. The company may use the money for legitimate business expenses. It does not have to leave the full amount untouched in the bank account.

Can I withdraw the paid-up capital after incorporation?

Not simply because you are the shareholder who contributed it. Once paid, the money belongs to the company. Returning capital to shareholders may require a formal capital reduction, share buyback or another legally permitted transaction.

Can I treat money transferred to the company as paid-up capital later?

The original purpose of the payment should be clear. A transfer recorded as a shareholder loan does not automatically become share capital. Converting a shareholder loan into equity normally requires the appropriate approvals, share allotment and ACRA filing.

Must paid-up capital be deposited into the company’s bank account?

The shareholder must genuinely provide the consideration stated as paid. Once the company’s bank account is available, cash capital would ordinarily be transferred into the company account and supported by the relevant records. The accounting treatment should remain clear where the company was incorporated before its bank account was opened.

Does a foreign-owned company need more than S$1?

Foreign ownership does not by itself create a general higher incorporation minimum. Separate requirements may apply to the company’s intended business activity, licence or the work pass required by the foreign director or shareholder.

Is S$50,000 required for EntrePass?

No. The former S$50,000 paid-up capital requirement was removed in 2017. Applicants must meet MOM’s current EntrePass eligibility requirements instead.

Is there stamp duty when new shares are allotted?

Share duty generally concerns the transfer of existing shares between parties. An allotment of new shares by the company is different from a transfer of existing shares. The allotment must nevertheless be properly approved and filed with ACRA.

Can paid-up capital be in a foreign currency?

ACRA allows share capital to be recorded in different currencies. The selected currency and corresponding share capital details must be correctly reflected in the company’s records and Bizfile filings.

Quick Reference

| Question | General Position |

|---|---|

| Minimum share capital at incorporation | S$1 for a company that requires share capital |

| Must the full amount remain in the bank? | No |

| May the company use the funds? | Yes, for legitimate company purposes |

| Does it directly affect corporate income tax? | No |

| Can it be increased later? | Yes, usually through a further share allotment or payment on partially paid shares |

| Can it be reduced later? | Yes, through a formal capital reduction process |

| Current EntrePass minimum | No prescribed S$50,000 paid-up capital requirement |

| Automatic Singapore Business Federation membership | Paid-up capital of S$500,000 or more |

| May licences or grants require more capital? | Yes, depending on the applicable scheme |

The appropriate paid-up capital depends on how the company will be funded, its intended business activities and whether any licensing or grant requirements apply. Leftright Corporate can assist with the initial share structure, incorporation and subsequent capital increases through our Singapore company incorporation services.